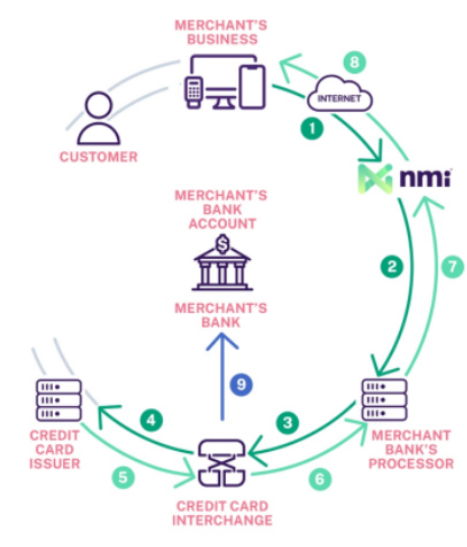

Firearm Ecommerce payment processing is a complex system that plays a crucial role in the success of any online business. For every transaction, there is a seamless flow of information across multiple layers, from the customer’s initial action to the final settlement. Understanding these steps is essential for merchants to optimize their payment systems and provide a secure experience for their customers. In this blog, we’ll break down the ecommerce payment lifecycle into simple steps, highlighting where NMI (Network Merchants, Inc.) fits into the process.

Step 1: Initiating the Firearm Ecommerce Payment

The ecommerce payment process begins the moment a customer decides to make a purchase, either in-store or online. In this first step:

- In-store: The customer physically hands their credit card to the merchant.

- Online: The customer enters their payment details, such as card number, expiration date, and CVV code, on the website’s checkout page.

When the customer submits their payment information, it is transmitted over the internet to NMI. NMI acts as the payment gateway, securely capturing and encrypting the payment data to prevent fraud or unauthorized access. This transmission is a critical step in the ecommerce payment lifecycle because it kicks off the verification process that will eventually lead to either an approval or a decline.

Where NMI Fits: At this stage, NMI serves as the initial point of contact that securely transmits the payment data from the merchant’s environment to the next step in the transaction. This seamless transfer ensures the customer’s information remains secure while being sent to the merchant’s payment processor.

Step 2: Transmitting to the Merchant’s Processor

Once NMI receives the payment details, the next phase in the ecommerce payment lifecycle begins. NMI securely routes the payment information to the merchant’s payment processor. The processor plays a crucial role in managing and forwarding the transaction data to the next destination: the card network.

The processor is essentially the middleman that facilitates communication between the merchant, the card networks, and the customer’s issuing bank. At this stage, the processor verifies that the payment details are correctly formatted and ready for the subsequent steps in the ecommerce payment process.

Where NMI Fits: NMI acts as the gateway that handles the secure transmission of payment data to the processor. Its role is to ensure that the merchant’s data is accurately and safely conveyed, maintaining a seamless payment experience.

Step 3: Routing to the Card Networks

In Step 3, the payment processor identifies the type of card being used (e.g., Visa, MasterCard) and sends the transaction to the corresponding credit card interchange network. The interchange network is a vital component of the ecommerce payment process because it manages the transfer of transaction data to the appropriate parties, applying transaction fees in the process.

The interchange network is responsible for routing the transaction details to the cardholder’s issuing bank. This part of the lifecycle is where the information starts its journey toward authorization. It’s essential to note that the transaction data flows through multiple channels at this stage, and the interchange network ensures that it is transmitted correctly and securely.

Explanation: NMI’s gateway services facilitate the connection between the processor and the interchange network. Without this smooth handoff, the transaction could encounter delays or security issues, which could negatively impact the customer’s ecommerce payment experience.

Step 4: Sending to the Issuer/Cardholder’s Bank

In this phase of the Firearm ecommerce payment lifecycle, the interchange network routes the transaction details to the cardholder’s issuing bank. The issuer is the bank that provided the customer with their credit card. This step is crucial as it determines whether the transaction can be approved or declined based on several factors.

When the issuing bank receives the payment request, it examines key aspects of the transaction:

- Sufficient Funds: It checks if the customer has enough available credit or funds to cover the transaction amount.

- Security Verification: The bank verifies the transaction for any red flags, such as unusual purchase patterns, location mismatches, or incorrect security codes.

- Card Status: The bank ensures that the card is active, not expired, and hasn’t been reported as lost or stolen.

After evaluating these conditions, the issuer decides whether to approve or decline the ecommerce payment. This decision is then sent back to the interchange network, accompanied by an authorization code that indicates approval or provides a reason for the decline.

Where NMI Fits: While NMI does not interact directly with the issuing bank, its role earlier in the process (by securely transmitting the payment details) enables this decision-making step. NMI ensures that the initial data is accurate, which helps avoid potential delays or errors during the issuer’s evaluation process.

Step 5: Decision Transmission to the Interchange Network

Once the issuing bank makes its decision, it sends an authorization response back to the interchange network. This response typically includes a code indicating either approval or the reason for a decline, such as insufficient funds or an invalid CVV code. The interchange network then routes this response to the merchant’s payment processor.

This step in the firearm ecommerce payment process is crucial for providing merchants with real-time feedback. A prompt and accurate response is necessary to enhance the customer’s experience and to help the merchant proceed with the next steps, whether fulfilling the order or addressing any issues that arise from a declined payment.

Where NMI Fits: NMI facilitates the flow of information between the processor and the merchant by capturing and relaying the response from the interchange network. By doing so, NMI ensures that merchants are promptly informed of the transaction status, allowing them to take appropriate actions, such as completing the sale or notifying the customer about any payment issues.

Step 6: Processor Receives the Response

After the interchange network routes the issuer’s decision, it sends the response to the merchant’s payment processor. The processor’s role here is to capture the response (approved or declined) and prepare to relay it to NMI. This communication is key in the ecommerce payment process, as it provides real-time feedback to both the merchant and the customer.

In an approval scenario, the transaction amount is essentially earmarked by the issuer, signaling that funds are available for the merchant. Conversely, if the transaction is declined, the processor forwards the reason provided by the issuer, such as “insufficient funds” or “incorrect CVV.” This clear communication ensures that the transaction’s status is accurately conveyed to the next participant in the payment chain.

Where NMI Fits: NMI acts as the conduit between the processor and the merchant. It receives the processor’s response and facilitates its delivery to the merchant’s interface. This rapid exchange of information is crucial for a smooth ecommerce payment experience, allowing merchants to quickly respond to approved payments or handle declined ones efficiently.

Step 7: Passing the Response to NMI

When the processor sends the transaction’s status to NMI, NMI then displays this response to the merchant, whether in-store or online. If the ecommerce payment is approved, NMI updates the merchant’s system, confirming that the purchase can proceed to the order fulfillment stage. For an online environment, this step often appears as a confirmation page for the customer, signaling that their payment has been successfully processed.

In the event of a decline, NMI communicates the issue back to the merchant, which can then take appropriate steps, such as notifying the customer or requesting alternative payment methods. This stage is where NMI adds value by streamlining the communication flow between the various entities involved in the ecommerce payment lifecycle.

Key Point: NMI’s interface makes the transaction status immediately accessible, reducing wait times for customers and allowing merchants to respond proactively to any payment issues. This responsiveness is vital for maintaining a positive customer experience and can help reduce the likelihood of cart abandonment in ecommerce scenarios.

Step 8: Displaying the Response to the Merchant and Cardholder

After receiving the transaction status from the processor, NMI displays the result to both the merchant and the cardholder. In an ecommerce payment environment, this step typically involves:

- For the Merchant: Updating the point-of-sale (PoS) or ecommerce system to indicate whether the payment was approved or declined.

- For the Cardholder: Displaying a confirmation page if the payment is successful, or an error message with guidance if the payment is declined.

By providing an instant update, NMI ensures the merchant can immediately proceed with order fulfillment or take action to resolve any payment issues. This quick feedback loop is essential in ecommerce payments, as it allows merchants to provide a seamless checkout experience and reduces the risk of cart abandonment.

Where NMI Fits: NMI’s system acts as the interface that merchants rely on for real-time transaction updates. This visibility is crucial for managing inventory, order processing, and customer communication, particularly in a fast-paced ecommerce environment.

Step 9: Settlement of Multiple Transactions

The final step in the ecommerce payment process is settlement, where all transactions processed during the day are aggregated and sent back to the merchant’s processor. During this phase:

- Processor’s Role: The processor calculates the total funds from approved transactions and sends this data to the merchant’s acquiring bank.

- Acquiring Bank: The acquiring bank then facilitates the transfer of funds to the merchant’s bank account, typically within 1-3 business days.

Where NMI Fits: NMI’s involvement ends with the completion of transaction processing and communication to the merchant. It does not have visibility into the actual settlement and funding processes, as these occur between the processor and the acquiring bank. However, NMI’s accurate and timely transaction management is vital for ensuring that the correct amounts are ultimately settled and deposited into the merchant’s account.

Key Point: Although NMI doesn’t directly handle the funding process, its role in securely managing and transmitting transaction data ensures that settlements are conducted smoothly. This final stage closes the ecommerce payment loop, allowing merchants to receive funds for the goods and services they have provided.

Ecommerce payment processing involves a complex yet well-orchestrated series of steps, each crucial to completing a seamless transaction. From the moment a customer initiates a purchase to the final settlement of funds, multiple entities—such as NMI, processors, card networks, and issuing banks—work together to ensure that payments are processed securely and efficiently.

NMI plays a central role in this lifecycle. Acting as the gateway, it facilitates the secure transmission of payment data, interfaces with the merchant’s payment processor, and provides real-time responses to both merchants and customers. While NMI doesn’t handle the final settlement of funds, its role in managing the flow of information is vital for the successful completion of ecommerce payments.

Understanding each layer of this payment process enables merchants to optimize their checkout experiences, reduce payment-related issues, and build trust with customers. With NMI’s secure and streamlined services, merchants can focus on growing their business while ensuring a smooth and reliable payment experience for their customers.

In today’s fast-paced ecommerce landscape, being well-versed in how payment transactions work gives merchants a strategic advantage, allowing them to enhance both operational efficiency and customer satisfaction.